2024 State of the ConTech Ecosystem - Funding Numbers & Investor Outlook

A review of the funding activity in 2024 and key takeaways from Zacua Ventures' 2025 Investor Outlook

For the last year, on Last Week in ConTech, we’ve been tracking startups which impact the way in which the construction industry operates and functions. This information has allowed us to have a broad view and understanding of the market and undertake a review on the state of funding for the Construction Technology ecosystem.

The challenge we’ve found however with tracking ConTech startups is there is no unified definition on what a ‘ConTech’ startup is.

This is further compounded by the broad nature of construction, which, rather than being a clearly unified industry, is made up of distinct sectors (e.g residential, commercial, infrastructure and industrial) which are varied and unique to each other.

What is unifying is the general ‘process of construction’ and the project stakeholders. Based on this thinking and in conjunction with Zacua Ventures, we applied a more stringent filter on the startups featured to incorporate in our ‘State of Funding’ analysis.

A ConTech startup was defined as any startup which is developing a technology which impacts the construction value chain. This could be from land development to design, engineering, planning and construction.

The definition also covers retrofitting, remodelling, infrastructure and building operations, maintenance, material manufacturing, logistics, installation, and end-of-life processes like recycling.

Some notable exceptions to this definition which were excluded in this analysis were:

Building management systems / operations phase solutions

This wasn’t included as it was considered ‘Proptech’ though infrastructure / grid asset management and inspection startups were included.Heat pump suppliers

These were excluded unless the startup had inhouse installers (a subcontractor e.g 1komma5°).Startups which build charging infrastructure.

Hyperscalers (companies building large scale data centres and offering computing and storage services)

Debt rounds were excluded (grants were included)

Additionally, a ConTech startup may not sell exclusively to the construction industry and may also operate in adjacent sectors e.g. Weavix (smart radios used in frontline industries such as construction). This definition may be broader than those used by other companies which track the ecosystem and therefore result in a higher number of deals. However, the intention is to highlight startups that engineers and industry professionals can actively use to improve their day-to-day work.

In the desire for transparency and unity, all the deals and calculations included in the analysis can be accessed here (for readers to view) and there is a column outlining why it was included allowing readers to make their own judgements and analysis on the inclusion, categorization and relevance.

Let’s get into the review.

Contents

ConTech investment in 2024

Investment by Region

Investment by Categories

Number of Deals

Amount of Funding

Top Category by Region

2025 Investor Outlook

(powered by Zacua Ventures)Investment Expectations

Investor Concerns

Valuation Expectations

Investment Focus Areas

Investment Criteria

Key Investor Survey Takeaways

2025 Key Themes

Construction labor shortage

Climate adaption of existing infrastructure

Data Centre investment

Transmission infrastructure solutions

Alternative Supply Chains

Disclaimer: The purpose of this database is knowledge sharing and entertainment, this is not investment advice and is based on public information and investment activity provided by investors, tech companies, and third-party organizations. While efforts have been made to ensure the accuracy of the data, there may be mistakes. Readers are advised to review the data and fact check. Additionally, we do not endorse companies for investment purposes. The information provided should not be used to make any investments or financial decisions. Please consult an investment specialist before investing.

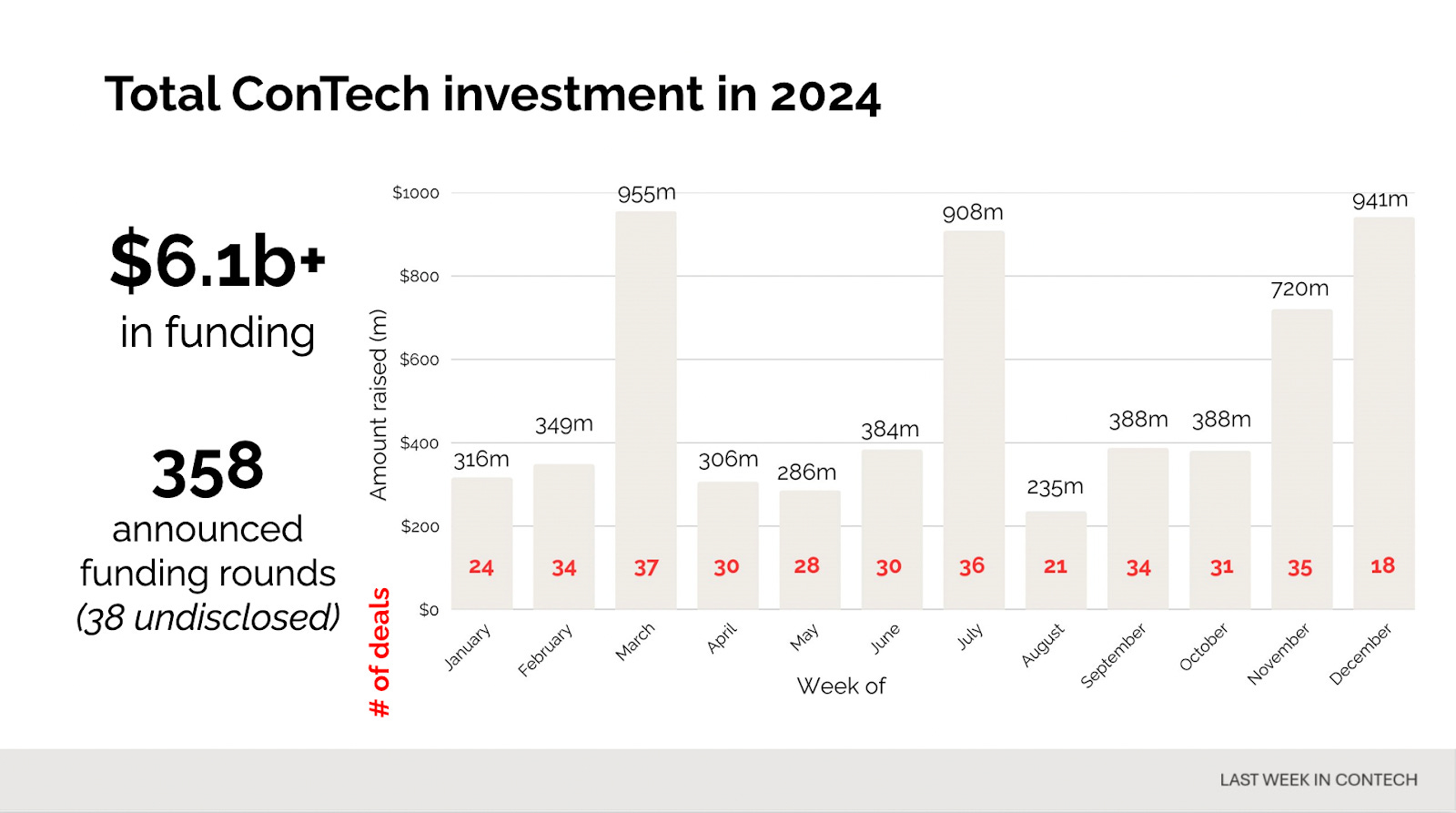

ConTech investment in 2024

In 2024, the industry received over $6.1 billion (USD) in venture and grant funding. This funding went to 320 startups with a further 38 receiving an undisclosed amount of investment.

*Startups that raised multiple rounds last year—such as a venture round followed by a publicly announced grant—were counted twice.. This can be see by applying a conditional formatting filter to the raw data.

Construction Tech continues to grow as a proportion of total venture funding. This year it accounted for 1.97% of the total $314 billion deployed by venture capital firms. With the construction industry accounting for 13% of global GDP (McKinsey, 2020), there is still upside and potential for growth.

Investment by region

North America was the primary region for ConTech investment, capturing 59.4% of total funding ($3.67 billion). Together, North America and Europe accounted for over 85% of global investment.

In terms of the number of deals, North America remained the leader, accounting for 42.7% (153) of total transactions, followed by Europe at 37.9% (136). This gap between total funding and transaction count suggests a rise in early-stage investment rounds in Europe. In general, the US market is more mature (more growth size rounds) and round sizes tend to be larger.

The United States was the primary country for both the number of deals (152) and amount of funding ($3,668m). The United Kingdom, Australia and Germany were the next 3 countries for investment activity.

Investment by Category

Each of the investments were broken into subcategories which can be seen in the analysis.

Number of Deals

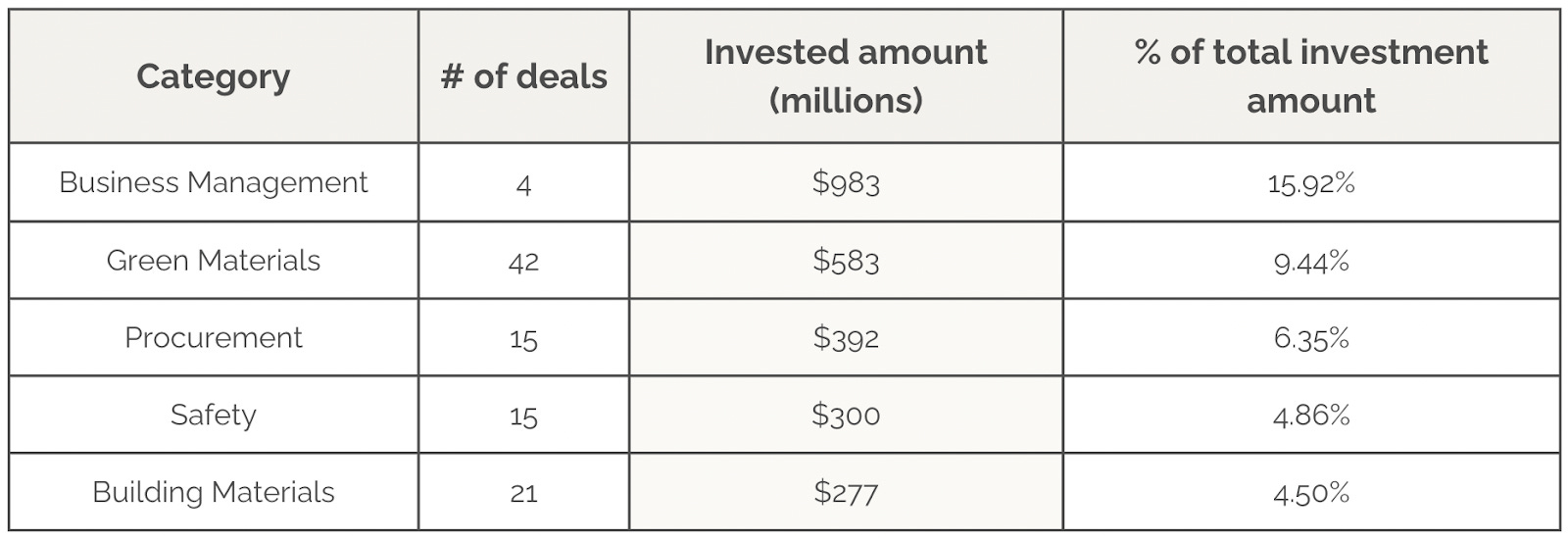

Green materials and the building material category more broadly received the highest total number of transactions at 42 and 21 deals respectively reflecting continued investor interest in the sector. This was followed by construction management (21), procurement (15) and safety (15).

An additional category of interest is AI.

AI startups in construction were defined as companies driving foundational change through AI. For example, Trunk Tools, which is building an ‘AI brain,’ and Mode, which is developing a generative AI assistant that connects to sensors and cameras for real-time analysis, fit this category.

However, most startups use AI to enhance business processes rather than as their core innovation. For instance, BuildPass is developing an AI-driven platform for construction management and was therefore classified as a ‘Construction Management’ solution.

This categorization framework, based on use cases, highlights that AI’s value often lies in its application to specific business challenges and was used as the intention is to highlight how a new solution can be used by an industry professional.

Within this categorization of AI, there were 8 funding rounds amounting to a total of $64.5 million.

Amount of funding

In December 2024, ServiceTitan went public, raising $625 million. As a result, Business Management became the most funded sector of the year ($983), followed by Green Materials ($583m), Procurement ($392m), Safety ($300m) and Building Materials ($277m).

The significant investment in Green Materials and Building Materials likely reflects growing investor interest driven by climate reduction policies. Additionally, these sectors may require larger funding rounds due to the capital-intensive nature of scaling manufacturing capacity and producing stock

Investment by stage has not been analysed as the amount of publicly available data on stage (e.g seed, Series A etc) was limited. Only 117 of the 361 deals tracked provided this data.

Top Category by Region

The top category in North America and Europe for the number of deals was Green Materials indicating strong investor interest in decarbonizing embodied emissions in construction.

This is surprising as the policy environment in Europe is more conducive to building decarbonization when compared to the US (other than California and New York).

The top category by investment amount varies across the regions and was skewed by large individual rounds (e.g ServiceTitan IPO).

The number of deals in South America (5), Africa (2), and MENA (8) was quite low and distributed quite evenly across categories, hence it is not included in the below table.

2025 Investor Outlook

To gauge the investment outlook for 2025, Zacua Ventures conducted a ConTech investor survey capturing insights and expectations from 130 unique investors. This annual survey, first launched in 2023 and their results and analysis are being shared publicly first on Last Week in ConTech.

The surveyed group comprises venture capital funds (VCs) and corporate venture capital funds (CVCs) who are primarily focused on early stage construction technology investments with a global investment scope.

Investment Expectations

Investors signaled their intent to either increase (47%) or maintain (43%) their capital deployments in 2025 (90% in total, compared with 88% in 2024 and 78% in 2023).

This trend reflects the recovery in early stage ConTech investment sentiment from the sharp decline in 2022 indicating growing confidence in the market’s long term potential.

There is a key distinction between VCs and CVCs with the latter having adopted a more cautious and conservative approach with the majority (51%) seeking to maintain investment levels while the majority of VCs (60%) are expecting to increase their investments.

Investor Concerns

Investors were surveyed on their concerns for the sector.

Market uncertainty continued to be the top concern for investment (37%) but is markedly down from 2023 (61%). Similarly, concerns about valuation corrections have followed a downward trend with 38% in 2023, 32% in 2024 and only 19% in 2025.

On the other hand, availability of funds has become a growing concern, with a steady increase in investor apprehension since (29%, 31% and 33%). CVCs appear more constrained, with 35% expressing this concern compared to 29% of VCs.

Valuation Expectations

Investors expect valuation to remain constant or increase in 2025 (79%). This is a sharp improvement compared to 2024 (55%) and (29%) in 2023.

Given this data, along with macroeconomic trends indicating higher ConTech adoption, positive outlook for the construction industry as well as increasing levels of M&A, it seems likely that we are past the trough in ConTech valuations that occurred in 2024.

Investment Focus Areas

Investors are incredibly interested in AI with 56% planning to allocate more funds in 2025 compared to 2024. This replaced Sustainability as the focus area, declining from 58% in 2024 to 48% in 2025.

Additionally, Robotics emerged as an area of increased interest (34%, up from 25% in 2024).

Innovations in robotics including higher flexibility, multi-tasking capabilities and reduced set up times align with macroeconomic trends such as skilled labor shortages, paving the way for broader adoption in construction.

Investment Criteria

Investors noted Team, Traction and Differentiation as the key factors when evaluating startups.

Interestingly, there was a separation in considerations between VCs and CVCs. While both prioritize the top 3 considerations there difference was:

VCs

Focus on Team quality, Traction & Differentiation and Growth Potential (Market Size & Go-to-Market strategy).CVCs

Place greater emphasis on Product / Tech, Efficient Growth (burn rate) and Strategic Fit (alignment with their business)

Key Investor Survey Takeaways

This survey has been run for 3 consecutive years. Based on the results, the key changes forecasted can be summarised as:

Increased optimism

Investment sentiment has improved with stabilized valuations and increased capital deployment plans.Expectations on valuation recovery

After 2 years of declining valuations, the trough appears to have passed with a conservative increase expected in 2025.Shift in investment criteria

Differentiation has become a critical factor in investment decisions, reflecting a competitive market for standout innovations.

Technology focus evolution

There is a shift from sustainability to productivity-oriented technologies such as AI and robotics translating to a market preference for immediate ROI and efficiency.

The full investment survey report by Zacua Ventures which includes further analysis such as regional technology focus can be found here.

2025 Key Themes

Anticipating the future and the sectors of focus or growth is a difficult challenge especially in this volatile geopolitical environment.

As Mike Pompeo, former US Secretary of State, warned investors it has become ‘impossible to separate geopolitical risk from capital allocation.’ The construction tech industry is just as affected by this with examples such as rising US-China tensions or recent tariffs brought by Trump on Mexico and Canada impacting supply chains and material sourcing.

One small scale example is the US considering banning Chinese DJI drones on national security grounds. This could have repercussions on the use of drone based reality capture solutions and drive investment into alternative manufacturers, who instead of selling to businesses or integrating with providers such as DroneDeploy, may vertically integrate and enter the market which Skydio, an American manufacturer of drones is undertaking.

It is therefore important to understand both the wider geopolitical context and the shifting policy landscape as well as deeply understand the construction industry's pain points when reviewing themes.

Given these challenges, at Last Week in ConTech, we are interested in the following themes:

Construction labor shortage

Climate adaption of existing infrastructure

Data centre investment

Transmission infrastructure solutions

Alternative supply chain / procurement solutions

For each of these themes we will provide an overview and our hypothesis on why we are interested and tracking them. Note: This is not investment advice (please see disclaimer above).

Construction labor shortage

The Associated Builders and Contractors (ABC), found that approximately 439,000 net new construction jobs are needed this year in the US. For every $1 billion in construction spending, 3,550 new jobs are needed.

The industry does not have the workforce to meet this demand. It’s led to a rise in average hourly earnings throughout the industry, up 4.4% over the past 12 months, outpacing earnings growth across all industries.

This high willingness to pay combined with immense demand will continue to increase the industry's interest in robotic solutions to augment construction workers.

The challenge so far has been in the go-to-market motion with GCs and subcontractors generally unable to justify the high capex cost and variable utilization.

An rising model is integration of the robots into the industry’s existing delivery model. For example, Monumental is a bricklaying subcontractor staffed entirely by robots. By vertically integrating product development and delivery, they are able to integrate into a GC’s tendering process for subcontractors.

At the end of the day the industry values results and compliance caring less about how the service was delivered.

This trend of robotic solutions being used to augment their labor is likely to continue as demand and real wages continues to increase. As a result, the supply of robotic solutions will likely grow, improving unit economics and making them more viable.

Climate adaption of existing infrastructure

For years the insurance firms have been reducing coverage in areas prone to natural disasters, citing an increase in claims due to climate change.

This issue has been in the national spotlight with the recent Los Angeles wildfires costing up to $164 billion in property and capital losses.

Asset owners are beginning to recognise the risk posed to their infrastructure portfolios recognising the need for proactive mitigation and adaptation. Additionally most infrastructure built in the 1900s to early 2000s used climate data from the mid-1900s, lacking the ability to withstand current changes in both intensity and frequency of extreme weather events.

It’s making major news coverage with CNBC highlighting that property owners are recognizing that they must make changes to improve resiliency, maintain insurability, and lower costs such as replacing wood fencing with steel to withstand natural disasters.

Recognising this need, the Biden Administration allocated $50 billion for climate resilience and adaptation as part of the Bipartisan Infrastructure Law and Inflation Reduction Act.

Given the rising interest, solutions associated with scenario planning of natural disaster risk to portfolios and which adaptations to prioritize will become increasingly valuable.

Additionally, in the shorter term, there may be an uptick in funding for solutions such as Kahi and Rebuild which support restoration contractors hired by insurance companies post natural disasters.

Data Centre investment

According to CBRE, there are 4,750 data centres under construction in the US in 2025.

When combined with Trump’s recent announcement of $100 billion of investment in computing infrastructure by OpenAI, Softbank and Oracle and Big Tech’s (Amazon, Alphabet, Meta and Microsoft) forecasted over $300 billion in capex spend for 2025 (up from $155b in 2023, $246b in 2024) driven by AI needs, it represents significant growth.

These investments are driven by growing demand for AI and the U.S.’s desire to control and lead in what they see as a critical technology. The level of spending is reminiscent of cold war era spending where the government and private sector committed substantial resources to ensure leadership in technology deemed critical for economic and national security.

The growing demand in the sector may result in generic solutions such as construction management, procurement or safety solutions being tailored to contractors servicing the data centre construction market.

Given the growth and scale of this sector, tech solutions that gain traction among data centre contractors could see accelerated adoption, expanding in parallel with the sector’s growth.

Transmission infrastructure solutions

Global electricity demand is predicted to increase at a faster rate over the next 3 years.

This is impacted by two major factors:

Electrification and AI energy use has increased demand.

Renewable energy sources and the decommissioning of polluting energy infrastructure has changed supply.

Modern grid infrastructure was designed for centralized scalable power generation (power plants). The new grid is different with intermittent supply and is increasingly distributed with local solar and batteries resulting in an orchestration (coordination) problem.

The challenge is that renewables location is dictated by the natural environment. While we have become better at constructing solar parks or wind farms, the challenge is connecting them to the grid.

The reason why is that in the US, before a new power plant is connected to the grid, operators must evaluate whether the existing system has enough capacity to handle the change and determine what upgrades might handle the increased load.

As the studies are being undertaken, the project sits in the interconnection queue. There are currently over 11,000 projects in the queue, amounting to a generation and storage capacity of ~1,900 gigawatts. This is double the generation capacity in the US.

Given the difficulty with permitting new transmission line infrastructure (takes ~4 years) solutions which increase the capacity of existing infrastructure or help assist with the maintenance and uptime of existing infrastructure will be valuable.

Examples include Veir, which replaces conventional power lines with superconductors, and Smart Wires, which helps utilities maximize existing infrastructure through grid-enhancing technologies and services.

Alternative Supply Chains

Rising tensions and trade wars between China and the US appear to be the norm rather than the exception. This tension has led to a wave of nearshoring, which is the practice of moving business operations to a nearby country to reduce supply chain risk and increase resilience.

This practice will extend to building materials as the West seeks alternative and cheaper suppliers. The challenge in other low cost markets such as South East Asia, South America or India is that the market is fragmented and does not meet Western material specifications or quality requirements.

There is an opportunity for startups to specialise in cross border procurement and helping small scale material suppliers in low cost regions connect to Western construction companies. The procurement startup (or marketplace) would ensure quality of the material and handle logistics providing an alternative supply chain to China for Western companies.

An example is Latii which is a managed marketplace and supply chain automation tool for construction materials, allowing U.S. customers to source high-quality, price-competitive, precision-made fenestration products from Latin America, Southern Europe, and North Africa.

They provide access to alternative supply chains previously inaccessible to the U.S. market.

The construction tech ecosystem continues to remain robust and is becoming an ever increasing proportion of the general venture landscape. While the term ‘ConTech’ is not as prominent as ‘FinTech’ or ‘HealthTech,’ the current trajectory suggests that we are moving towards an inflection point, where construction tech receives a large proportion of the funding and provides solutions which meaningfully impact the way in which we deliver projects.